AI in Financial Services: How Firms Reduce Fraud Risk

Struggling with fraud detection? See how AI in financial services reduces risk, detects fraud in real time, and improves decision-making fast.

I’ve worked with financial teams who believed their fraud systems were working, until one incident exposed the gap. This is where AI in financial services is transforming fraud detection and risk management.

A transaction was flagged, but only after the money had already moved.

That delay is where most losses happen.

If you're dealing with rising fraud alerts, too many false positives, or slow manual reviews, you’re already seeing the limitations of traditional systems.

This is exactly where AI in financial services starts making a measurable difference.

What is AI in Financial Services for Fraud and Risk?

AI in financial services helps financial institutions detect fraud, reduce financial risk, and identify suspicious behavior in real time using machine learning and predictive analytics.

-

Unlike rule-based systems, AI adapts continuously.

-

It doesn’t just detect fraud; it learns how fraud changes.

Why Traditional Fraud Detection Systems Fail

Most legacy fraud systems depend on fixed rules. If a transaction crosses a threshold, it’s flagged. If not, it passes. Modern financial fraud no longer follows predictable transaction patterns.

I’ve seen cases where attackers split transactions into smaller amounts to stay below detection limits. The system sees normal behavior. The business sees losses later.

According to McKinsey, financial institutions lose up to 5% of annual revenue to fraud. That’s not just a security issue; it’s a direct hit on profitability.

More importantly, these systems:

-

Generate high false positives

-

Require heavy manual verification

-

Fail to adapt to new fraud tactics

This creates operational pressure, especially for growing financial teams.

How AI Fraud Detection in Financial Services Actually Works

With AI fraud detection in financial services, the approach shifts from rules to behavior.

Instead of asking:

“Does this transaction match a rule?”

AI asks:

“Does this behavior match the user’s normal pattern?”

It analyzes:

-

Transaction history

-

Device and location patterns

-

Spending behavior

-

Timing anomalies

For example:

-

A user suddenly logging in from a different country

-

Multiple rapid transactions within minutes

-

Spending patterns that deviate from historical behavior

AI flags these instantly.

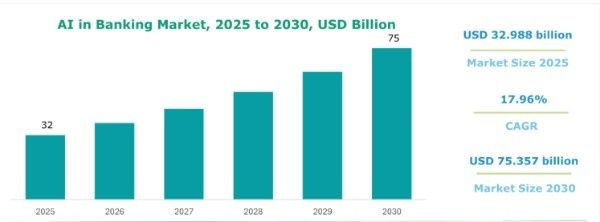

According to Statista, AI adoption in banking is projected to exceed $64 billion by 2030. This shows how quickly financial institutions are moving toward predictive systems.

Source link:- https://www.knowledge-sourcing.com/report/artificial-intelligence-ai-in-banking-market

Fraud Detection is One Layer - Risk Management is the Bigger Win

Fraud detection solves immediate threats.

But AI risk management in finance is where long-term value comes in.

This includes:

-

Real-time risk scoring

-

Predictive threat modeling

-

Automated decision-making for low-risk transactions

In one BFSI project I worked on, AI reduced false fraud alerts by 32% within 90 days. The team shifted focus from reviewing every alert to only handling high-risk cases.

That’s where efficiency improves, not just detection.

Business Benefits of AI-Based Fraud Detection

Financial institutions are increasingly adopting AI because traditional fraud systems struggle to manage modern transaction complexity and evolving fraud patterns.

Financial institutions are increasingly adopting AI because traditional fraud systems struggle to manage modern transaction complexity and evolving fraud patterns.

AI helps financial institutions:

-

Reduce false positives: Teams spend less time reviewing legitimate transactions

-

Improve detection speed: Fraud is identified in real time, not hours later

-

Lower operational costs: Less manual intervention reduces overhead

-

Enhance compliance: AI supports AML and KYC processes with better accuracy

-

Improve customer trust: Faster and safer transactions improve user experience

According to Gartner, by 2026, over 80% of banks will adopt AI-driven fraud detection systems.

This means traditional systems will struggle to keep up with both scale and expectations.

Traditional vs. AI-Based Fraud Detection

|

Aspect |

Traditional Systems |

AI-Based Systems |

|

Detection Type |

Rule-based |

Behavior-based |

|

Speed |

Delayed |

Real-time |

|

Accuracy |

Limited |

Continuously improving |

|

Adaptability |

Static |

Learns over time |

|

Manual Effort |

High |

Significantly reduced |

This shift is not incremental; it’s structural.

How Firms Reduce Fraud Risk Using AI in Financial Services

From real implementations, AI doesn’t sit in isolation. It operates across multiple systems:

1. Transaction Monitoring

Real-time detection of suspicious activities using anomaly detection.

2. Customer Behavior Analysis

AI studies how users interact with financial systems and flags unusual patterns.

3. Fraud Prevention Systems

Blocks or pauses high-risk transactions automatically.

4. Compliance Automation

Supports KYC (Know Your Customer) and AML (Anti-Money Laundering) processes.

This is where AI services for financial institutions become critical, because integration defines success.

Where AI Implementation in Banking Goes Wrong

Most AI failures I’ve seen are not technical, they’re strategic.

1. Starting with tools instead of problems

Teams invest in AI without defining what fraud or risk they’re solving.

2. Poor data quality

AI trained on inconsistent or incomplete data leads to inaccurate predictions.

3. No system integration

AI tools run separately from core banking systems, limiting impact.

4. Expecting instant ROI

AI needs training, iteration, and refinement.

According to Harvard Business Review, nearly 70% of AI initiatives fail to deliver expected outcomes. In financial services, this usually means wasted investment without measurable results.

AI Implementation Strategy for Financial Services

From experience, successful implementations follow a clear pattern:

-

Start with one high-impact use case (fraud detection or risk scoring)

-

Integrate AI into existing workflows, not as a separate layer

-

Use real transaction data for continuous learning

-

Measure performance before scaling

This is where AI consulting plays a key role.

Because choosing the right use case matters more than choosing the tool.

Top Challenges in Fraud Detection for Financial Services

If your current system flags too many false alerts, detects fraud too late, or depends heavily on manual reviews, the issue isn’t detection, it’s the approach behind it.

1. High False Positives Slow Down Operations

Most rule-based systems generate large volumes of alerts, many of which turn out to be legitimate transactions. This forces teams to spend hours reviewing non-issues, increasing operational costs, and delaying responses to real threats.

2. Delayed Detection Increases Financial Risk

Traditional systems often detect fraud after transactions are completed. By the time alerts are triggered, the financial damage is already done.

3. Lack of Behavioral Intelligence

Fraud patterns are no longer predictable. Static rules cannot adapt to evolving tactics like micro-transactions or identity masking.

4. Heavy Dependence on Manual Processes

Many financial institutions still rely on manual verification for flagged transactions. This slows down decision-making and increases the chances of human error.

5. Poor System Integration

Fraud detection tools often operate in silos, disconnected from core banking systems, CRM platforms, or compliance tools. This lack of integration prevents a unified view of risk and limits the effectiveness of detection strategies.

6. Inability to Scale with Transaction Volume

As digital payments grow, transaction volumes increase significantly. Traditional systems struggle to process large-scale data in real time, leading to missed fraud signals or delayed responses.

FAQs

1. How is AI used in financial services for fraud detection?

AI analyzes transaction patterns, user behavior, and anomalies in real time to detect and prevent fraudulent activities before financial loss occurs.

2. Can AI reduce financial risk in banking?

Yes. AI predicts risks, assigns real-time risk scores, and automates decision-making, helping financial institutions minimize exposure.

3. What are the benefits of AI in financial services?

AI improves fraud detection, reduces manual work, enhances accuracy, lowers costs, and strengthens compliance processes.

4. Is AI implementation in banking difficult?

It depends on the strategy. With proper data, integration, and use case selection, implementation becomes more efficient and scalable.

5. How long does AI take to show results in financial services?

Initial improvements can be seen within 2 - 3 months, especially in fraud detection accuracy and reduction in false positives.

Get Better Fraud Detection Results with AI

Fraud is changing faster than most systems can handle.

The difference is not who detects fraud, but who detects it first.

AI gives financial institutions that advantage, but only when implemented correctly.

Start with one use case.

Fix one gap.

Measure the impact.

Then scale.

Fraud patterns are evolving faster than traditional financial systems can respond. AI-driven fraud detection helps financial institutions identify suspicious behavior in real time, reduce false positives, and improve operational efficiency across risk management processes.

Businesses that approach AI implementation strategically, starting with focused use cases and scalable integration, are more likely to achieve measurable improvements in fraud prevention and financial risk management.